Fulcrum Analytics:

New software tools give warranty and service contract providers new insights into cost, revenue, and profitability. But those who use them won't talk about them, to preserve the competitive advantage these analytical tools give them.

There are retailers that use a simple approach to extended warranty pricing: all products selling for more than $1,000 have service plans priced at $79. Everything selling for under $500 have service plans priced at $29. Everything in between is covered by $59 service plans.

And then there are retailers that micro-manage extended warranties for every model and every brand, matching the price of a service plan to the expected cost, using historical data and analytics to adjust premiums up or down. Behind the scenes are databases and algorithms that help to improve the precision and reduce the uncertainty of the forecasts.

Some retailers put such systems together on their own, or with the help of their extended warranty administrator or underwriter. Others bring in a specialist firm such as Fulcrum Analytics Inc. (a Warranty Week sponsor), which is what Paul Swenson did when he ran the extended warranty programs of Circuit City Stores Inc. more than a decade ago.

"I managed Circuit City's extended service plans as VP of warranty administration for ten years," he said, until 2002. "And then after that I wanted some underwriting and additional administration experience, so I moved to Aon Warranty Group, and was president and CEO of Aon Innovative Solutions and was also an officer of Virginia Surety, the underwriting company."

Hiring Consultants

Swenson said he first heard about Fulcrum Analytics while he worked at Circuit City. Internally, he had hired some analysts and put them to work developing some product segmentation systems and customer segmentation systems for the aftermarket renewal business. But that effort seemed to be in need of some additional outside help, he felt, so he brought in Fulcrum co-founder Scott Morrison and his team. And they jointly began to delve deeper into loss cost analytics and sophisticated customer and product segmentation for the retailer's extended warranty business.

"And when I moved over to Aon Warranty Group," Swenson said, he brought Fulcrum with him, because internally, he said, "we needed the cutting edge analytics that Fulcrum had and we didn't, both for customer and product segmentation, and loss cost analytics. Nor did we have the level of direct marketing technology that we needed. So I brought Fulcrum into several of our relationships."

Then he left Aon in 2006 and went to work for Fulcrum itself, as president of its Fulcrum Warranty Solutions division. And in one lengthy afternoon discussion with its chief technology officer Richard Vermillion, Swenson described his vision for a software system that could help a retailer or a manufacturer examine past extended warranty sales and claims data and make forecasts about future profitability. Two weeks later, Vermillion came back with a prototype for a set of tools that eventually came to be called the eXclaim Intelligent Claims Analyzer.

"There was a clear need for it from our clients," Vermillion said, particularly one large manufacturer who was arguing with its underwriter as to whether extended warranty prices needed to be increased. "So they asked us just from our analytical capabilities to dive into it. And so we dove in, and thought it would be great if some of this was codified into a tool set, as opposed to us having to pull it all together each time."

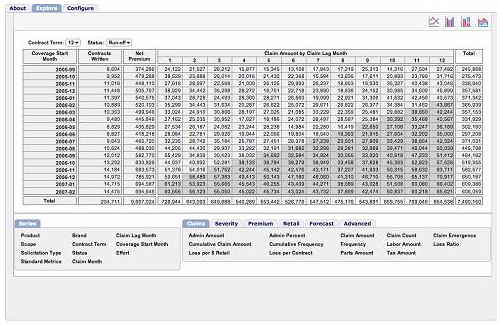

Vermillion said eXclaim is a mixture of databases and analytics with a front end that looks like an Excel spreadsheet. Although the front end interface looks simple, behind the scenes it's actually quite complex. "Some of our clients have tens of millions of claims that are stored in the database," he said. This allows the user to cut the data any way they like, be it by product line, model number, or one or more aspects of the warranty terms and conditions or claim type or cost.

Figure 1

eXclaim Intelligent Claims Analyzer

Source: Fulcrum Analytics

"Our goal with the front end was to make it look familiar, with a pivot table/spreadsheet type of format," Vermillion said, "so that you could go in and look at the various loss triangles and the tools that project out the bottom right-hand corner of the triangles to see what the future holds. But then also we tried to make it a general data exploration tool, to show you future claims and expected severity trends."

Not Sold As Software

Right now, Vermillion said, the eXclaim tools are better when used by Fulcrum's own analysts, rather than by the client's team. Fulcrum sells a service, and eXclaim is part of the tool set the company's own analysts use to get the job done. They're not out to sell software, or to shrink-wrap their expertise and license the code. Plus, it's not so simple to operate correctly, and it's somewhat easy to make a mistake that produces misleading results.

"Part of the issue is though we tried to make it easy enough so that clients can do it with a little training," Vermillion noted, "you still have to know a decent amount about how warranties are earned off, and you certainly have to know all the different parts of the accounting side: earnings patterns, claim emergence patterns, and the effect of different severity trends. We tried to couple the tools with some consulting and validation and some analytical hand-holding to make sure they're getting something that makes sense."

The eXclaim tools and the consulting services that come with it are aimed at retailers and manufacturers that participate in the product warranty and extended warranty industries, and particularly the chief financial officer, the risk managers, and the warranty and service contract program managers, Swenson said. Many times, Fulcrum sits with the CFO at the end of each quarter, making sure that the company's warranty reserves are at their optimal size. And sometimes, Fulcrum sits with either the internal controllers or external auditors that have the same questions as the CFO who must ultimately sign off on the financial figures.

Vermillion said the tools appeal both to those who want to do some exploring of the possibilities and those who want to simply fact-check their current status. Some want to drill down and look for problems, while others simply want to "run the books" once a month or once a quarter and generate some reports. And others want to put the data to work in terms of direct marketing, renewals, or customer relationship management.

He readily acknowledges there are other companies with tool sets that are optimized for product warranty or extended warranty analysis. But few do a good job of both, and none also do a good job at the marketing end of the business. "When you move into the extended service side, it's not the same as the limited," he said. "A lot of the same things apply, but how you market it, when you market it, and the manner in which you market it also matter, because it's not everybody who buys your product any more. And then you have to worry about things like adverse selection, or when you sell it to people out of coverage versus in coverage -- especially when it's in the aftermarket as opposed to the point of sale."

Anti-Campaign Management

"We don't believe in traditional campaign management," Swenson said. Under such a system, if five people bought a big screen TV on the same day at the same retailer and didn't immediately buy an extended warranty, they would all receive their first mailed solicitation on the same day. And if they ignored it, they would all receive their second solicitation on the same day.

In contrast, Swenson advises clients to customize each step using analytics. "We have analytics that take a look at household demographics and individual purchase histories with that particular retailer or manufacturer. We add loss cost analytics at the SKU level and score each customer/product combination into a different customer state, and would follow a different prescriptive but dynamic communication path. We have developed Customer State Machines to enable very sophisticated levels of customized marketing operations "

Swenson said some companies believe it's possible to get by with much less precise measurement and forecasting tools, particularly if rising revenues help to mask profitability problems. But some of those companies could also be fooling themselves. That rising revenue stream may also conceal the fact that a company's extended warranty program is "underwater" -- and losing money.

"You would be amazed at the number of manufacturers and retailers that we deal with, who by the way may have programs that are managed by third party companies, where they think they're optimizing the business, but what they're actually doing is maximizing revenue. And they have no idea how much money they're making, because either they don't take loss cost into account at all, or they take loss cost into account at an aggregate level."

One program Swenson's team recently began analyzing had $10 million in revenue per year, but was found to be operating at a $2 million annual net loss. "And they didn't know it," he said, "because they did not take into account loss cost at the appropriate level."

Besides understanding their own profitability, manufacturers and retailers also need to know if they're putting enough aside to pay future claims, Swenson added. "There's a real need, both for manufacturers and retailers who are carrying risk on their own books or who are using a third party underwriter, to understand loss cost at these kinds of detailed levels," he said. "For those carrying risk on their own books, they need to know if their in-force reserves are adequate to cover a liability that can extend out for 12 years. And their auditors have to sign off on that. And their CFOs and risk managers want to know."

Revenue Recognition Advantages

It's not all problem avoidance, however. There are some very real benefits to knowing when and how much to expect in claims in terms of revenue recognition. FASB Technical Bulletin No. 90-1, entitled "Accounting for Separately Priced Extended Warranty and Product Maintenance Contracts" mandates that premiums must be recognized gradually over the life of the contract, rather than all at once when the contract is first sold.

Specifically, the FASB accounting standard requires companies to recognize revenue using the straight-line method, "except in those circumstances in which sufficient historical evidence indicates that the costs of performing services under the contract are incurred on other than a straight-line basis."

Fulcrum's clients can demonstrate to auditors and regulators the true rate at which their extended warranty claims costs occur. Those that don't use Fulcrum or a competing analytics capability would be stuck using the straight-line method, because they simply don't have better data. One new client that Swenson declined to name was selling five-year extended warranties on a product that carried a three-year manufacturer's warranty. Amazingly, before Fulcrum came on board, they had been recognizing revenue at a straight-line rate of 20% per year, which meant they had recognized fully 60% of the contract revenue before they had to pay a single claim!

"That's not unusual," Swenson said. "You have to make sure you understand your claim emergence pattern, so you can set up your premium earning and amortization schedules to match those claim emergence patterns, or you can be in a lot of hurt." And that might not become apparent until sales decline, at which point it's even more painful to correct.

Analyzing Product Quality

On the flip side, a retailer could potentially use its loss cost data to either make better choices about what brands to stock, or to win price concessions from those brands that cost more to insure. In other words, the tools can show not only how much was made on the sale of the product, but also on the sale of the service contract. Reliable products that seldom break would have lower loss costs and would therefore have more profitable service plans, while those that break often might have service plans that actually lose money.

Swenson said that back when he first brought Fulcrum into Circuit City, he used to send some of these loss cost reports back to the manufacturers that they had determined were costing the retailer the most money in terms of warranted repairs. Three times -- once with a big screen TV manufacturer, once with a DVD player manufacturer, and once with a desktop PC manufacturer -- he was able to point out the brands and models that customers were bringing back most frequently. And he demanded reimbursements.

"I got seven-figure checks from three different manufacturers, and we got them to correct their manufacturing defect," he said. "And, we pointed out to one of them that they had a sound board problem before they even knew about it -- or would admit it!"

Since then, Swenson said Fulcrum has helped a manufacturer do the very same thing with a supplier that was selling it bad electrical motors. Fulcrum identified the problem part and determined the exact amount of money it was costing the OEM. The manufacturer took its case to the supplier, which not only paid for the problem but also corrected its manufacturing process so it wouldn't happen any more.

The problem is, while Swenson can talk all about the benefits of deploying Fulcrum's eXclaim Intelligent Claims Analyzer, he can't get any of his customers to agree to release their names. So it's uncertain whether even his former employers at Circuit City and Aon (now called The Warranty Group) are still Fulcrum customers. And it's unknown which particular manufacturers might be clients.

Unannounced Customer Signings

Swenson said Fulcrum has signed five major manufacturers and three retailers this year for eXclaim-style loss cost analytics services. None have allowed Fulcrum to announce the deals. "They don't want their competition to know how they're using us or how they're using these analytics, because for them it is a whole new level of profitability," he said.

Some don't want their names attached to articles that discuss the size or structure of industry or the risks inherent in extended warranties. Swenson said some don't want Fulcrum itself to be mentioned in articles, for fear that these secrets will get out. "But we're a relatively small company," he said. "And they understand that just as they have a business to run, so do we. But we would never do anything to breach their confidentiality."

Fulcrum, by calling attention to itself, focuses attention on the extended warranty industry. And this is an industry that doesn't want that attention. Usually, as the holidays approach the consumer magazines run an article saying "don't buy them" while the trade magazines theorize that extended warranty sales are somehow immune to economic cycles and technology trends. And then they're done for the year.

So along comes Fulcrum, touting the benefits of warranty analytics, but frustrated by an inability to name its best customers. And then others read about it, Google it, and pass it around, and the secret is a secret no more.

"It is a Catch-22," Swenson said, "because it is a service that's not rendered by many companies. It's not widely discussed and it's not widely known." But within a select group, it's something that can be discussed passionately, as he, Vermillion, Morrison, and Fulcrum president and CEO David King have demonstrated numerous times.

Planning for the Future

"We have manufacturing and retail customers. It runs the full spectrum. We have companies that are carrying the risk on their own books who need, for their own internal and external auditor purposes, to know that the reserve they are carrying on their balance sheet is appropriate for their in-force liability. They also want to make sure they understand if they are charging the right prices for the go-forward liability. Some of our partners have contracts that go out ten years. So they need to make sure the prices they are charging today will be appropriate to cover liabilities that go out that far. And then we have others that are using underwriters for a whole host of reasons -- income recognition, compliance, and so on -- that want to make sure they get a level of information they really can't get from their underwriters."

Some also want to double-check the rates their underwriters are charging, Swenson said. "When this business began to crank up several years ago, there wasn't a lot of book for some of these product categories," he said. So the underwriters were taking a bit more of a risk, because they didn't have the historical claims cost data to help them set rates. "Now, on most product categories, there are many years of history, and so it's not as risky as it used to be. And there are some manufacturers and retailers that are much smarter about their business than they were before," he added.

"When we sit down with the CFOs and risk managers, and they see what we have, it's real exciting because you can see them connecting the dots," he said. Twice in the last few months, in fact, he said CFOs who were just stopping in on one-hour pitch meetings have instead told their secretaries to cancel all their other meetings so they could stay longer to talk with Fulcrum. "They've had us stay for over four hours, because they were so excited about what they saw."

At the same time, Swenson said, he's not so concerned about potential customers "going to school" on them, because in this case knowing how it's done is not the same as being able to do it. "Usually, by the time they really understand the expertise that's needed, both from a technological standpoint and from a statistical/quantitative methods standpoint, they can see that it's not something you can do with some off-the-shelf software and a few analysts."