Consumer Reports' 2006 Extended Warranty Ad:

There was panic in the industry when one of the most trusted consumer advocates told its readers not to buy extended warranties. Ten years later, the magazine's advice is almost forgotten, and the industry is bigger than ever.

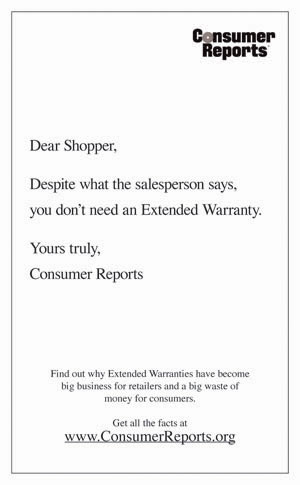

In a few weeks we'll be marking a very important anniversary in the service contract industry. Just as the holiday shopping season of 2006 was getting under way, a major consumer product ratings publisher told shoppers that extended warranties were a waste of money. On Tuesday morning, November 14, 2006, the USA Today newspaper carried on the back page of the "Money" section (page 10B), the following full-page ad placed by Consumer Reports magazine:

Reaction was swift. Some said both the frequency of breakdowns and the average cost of repair was higher than Consumer Reports was calculating, making service contracts a better value than was admitted. Others said it was simply a matter of price, in that nobody would deny the value of a service contract priced at 0% of the product's price (in other words, free).

A Matter of Price vs. Value

So there must always be a price at which a service contract is a break-even proposition for both buyer and seller. But at the other extreme, who would buy a service contract priced at 100% of the product's price (in other words, one for the price of two)?

Ten years later, we'd say the Consumer Reports advice of 2006 is now antiquated, in that it doesn't account for the growth of protection plans. And we mean not only the revenue growth, but also the growth in the breadth and depth of the protection plans, and what they cover.

Right around the time Consumer Reports issued its advice, accidental damage protection was being added into the coverage available for laptop and game console service contracts, along with technical assistance, installation advice, and access other member-only club benefits. So it covered not only mechanical breakdowns, but also droppage and trouble getting started.

A year after Consumer Reports issued its advice, Apple Inc. released the first iPhone. The wireless telephone companies offered not only break/fix coverage, but also accidental damage protection, and eventually, loss and theft insurance as well.

Two years after the newspaper ad appeared, Lehman Brothers collapses and nearly took the whole world with it. In early 2009, some of the car companies said they might not be able to pay claims on their factory warranties, and the U.S. government stepped in. Not long after that, some homebuilders went out of business, taking their warranties with them to the bottom. In 2011, Saab went bankrupt, and the dirty little secret of the warranty industry became clear: product warranties rarely outlive their manufacturer.

What Consumer Reports failed to note is that service contracts on new cars, new appliances, or new recreational vehicles usually have insurance backing of some sort, making them more dependable than product warranties in a deep recession. With poorly-financed import brands, or with precariously operative startups, you just can't depend on there being anybody still willing to pay product warranty claims in five, 10, or 25 years. With an insurance-backed service contract, there are laws protecting consumers.

Meanwhile, as recession gave way to recovery, the finance and insurance departments of the car dealerships began to broaden their protection catalogue. No longer covering just break/fix, they began offering plans that also covered dents, scratches, broken glass, tires, wheels, and upholstery. And they began selling plans that included both theft deterrence (etching the VIN into the glass and other spots) and financial loss protection (GAP waivers that paid off the loan on totaled cars).

Break/fix coverage, and the odds of it paying off for a consumer, is no longer the central issue. For mobile phone users, it's the peace of mind knowing that their $700 unit is covered if it's dropped, lost, or stolen. For vehicle service contract buyers, it's all sorts of ancillary and add-on coverages that fill in the gaps between warranties and auto insurance.

Evolution & Innovation

In Figure 1, we've charted this growth in capabilities for both smartphones and vehicles, illustrating how the protection plans have grown in both breadth and depth in the past decade.

Figure 1

Service Contract Evolution

From Break/Fix to Protection Plans

Extended warranties? We don't sell them any more. Instead, we sell protection plans that cover many additional perils besides break/fix. In fact, some of the wireless phone companies sell accidental damage and loss/theft coverage separately from break/fix policies, in case customers might prefer to buy one but not the other. The F&I offices sell GAP, dent, tire, wheel, etch, and other coverages completely separately from VSCs, and even the most stubborn buyers usually get at least one of them.

However, while the types of coverage are growing, so are the basic plans that Consumer Reports began to criticize a decade ago. In Figure 2 we've listed side-by-side the annual revenue estimates for the six largest segments of the U.S. consumer service contract industry in both 2006 and 2016.

Figure 2

US Service Contract Industry

Premiums Paid by Consumers, 2006 vs. 2016

(in US$ billions per year)

Warranty Week expects the total U.S. market for these six types of service contracts to top $42.2 billion this year, up 45% from $29 billion in 2006. In the past decade, only the computer OEM service contract segment contracted, and it did so only because sales of laptops, desktops, and notebook computers have given way to ever-smarter mobile phones, so unit sales are down, and so are the number of opportunities for retailers and PC manufacturers to sell service contracts for them.

Elsewhere, 10-year growth rates ranged from a below-average 25% for the vehicle service contracts to a far-above-average 258% rate for mobile phone protection plans. The other three industry segments grew slightly faster or slightly slower than the overall industry average.

Vehicle Service Contracts

One big reason the vehicle service contract industry grew only 25% from 2006 to 2016 was the depths of the downturn it suffered in between those years. The truth is, VSC sales were already declining by 2007 -- we just didn't know it was the start of a new trend.

In Figure 3, we've charted the annual totals for premiums paid by U.S. consumers for VSCs on their vehicles. And it's clear that the $13.7 billion total in 2006 would prove to be a high point as the entire car industry slipped into recession.

Figure 3

US Vehicle Service Contract Industry

Premiums Paid by Consumers, 2006 to 2016

(in US$ billions per year)

By 2009, the market bottomed-out at $9.9 billion. But it wasn't Consumer Reports that scared them away. Plain and simple, the dealership's F&I Office is the most likely place they'll buy a VSC. So if they aren't visiting and they aren't buying new cars, they also aren't buying VSCs.

By 2010, a slow recovery had started. And it continued. The market may now be leveling off again, with the 2016 total of $17.2 billion up by only $400 million from 2015. But the growth as measured from the depths of 2009 to the estimate for 2016 is 74%.

Electronics Service Contracts

Back in 2006, the laptop was hot, the flat screen television was hot, and the market for service contracts to protect them was hot. As was mentioned, by 2006 some retailers were offering accidental damage protection, so the customer's own clumsiness also entered into the equation. Even back then, it wasn't only about the frequency and severity of a break/fix incident versus the cost of the service contract. And with the more complex home theater systems, there could be installation and set-up issues that could be dealt with through a service contract call center.

Figure 4

Electronics Service Contract Industry

Premiums Paid by Consumers, 2006 to 2016

(in US$ billions per year)

Back in 2006, most of the service contracts on computers and home electronics were being sold by retailers such as Circuit City and Best Buy, and by manufacturers such as HP, Dell, and Apple. But back then, AppleCare covered Macs and iPods, because the iPhone wasn't launched until the middle of 2007.

Back then, the mobile phone protection plans sold by phone companies were a relatively small part of the industry. Offerings by Radio Shack and others still dominated. There were still a lot of flip-phones, and the low end mobile phones were viewed as disposable and not worthy of protection plans. But then the carriers began to offer loss and theft coverage, just as the phones became smarter, more expensive and more vulnerable, and by 2012 the carriers had almost a third of the total electronics protection industry.

Sales Channel vs. Product Type

In 2016, we expect the carriers to have about 45% of the electronics protection industry, while retailers have about 35% and the computer OEMs have only about 20%. But let's look at it a slightly different way. Instead of measuring the electronics service contract market by sales channel -- direct, retailer or phone company -- let's look at it by product covered -- mobile phone and everything else.

In Figure 5, when Radio Shack, Apple, Target or Best Buy sells a protection plan on a mobile phone, it's counted in the dark orange sector. When they sell a contract for a TV, computer, or other consumer electronics item, it's counted in the other category. When Apple or Dell sell a service contract for a computer, it's in the other category. But when Apple sells an AppleCare for an iPhone, it's in the dark orange sector.

Figure 5

All Sources of Mobile Phone Insurance

Premiums Paid by Consumers, 2006 to 2016

(in US$ billions per year)

It's the same overall totals as in Figure 4, but the product mix looks very different. Back in 2006, it was 80%/20% in favor of other products, in a $12.7 billion protection market. By 2011 it was 50%/50% in a $16 billion protection market. By 2014 it was 2:1 in favor of phones, and in 2016 we expect mobile phones to account for more than 67% of all electronics protection dollars in a U.S. market worth $21.3 billion.

Home Warranties & Appliances

As with mobile phones, there are multiple ways to buy protection plans for major appliances. Existing homeowners can choose to buy a home warranty that covers all the appliances in the house, including the heating and cooling systems, the kitchen and laundry appliances, and sometimes even the swimming pool and lawn equipment. Consumers pay roughly $500 per year, and then they pay $60 or so per service call.

Consumers can also choose to pay for service contracts at the point of sale, covering just the appliance they're buying. Sears, Home Depot, and Lowe's get most of these contract sales, because they have the first and best opportunity to convince the customer they need a protection plan.

In Figure 6, we've charted these two different ways a consumer can protect their major appliances: home warranty and retail. Back in 2006, the total appliance protection market was $2.5 billion, split 55%/45% in favor of the home warranty segment.

Figure 6

Home Appliance Service Contract Industry

Premiums Paid by Consumers, 2006 to 2016

(in US$ billions per year)

It hasn't changed much, though the segments have continued to grow, even through the depths of the recession. Combined sales of home warranties and appliance service plans surpassed $3 billion in 2013 and had reached $3.5 billion by last year. In 2016, we expect additional growth, with the industry reaching $3.7 billion. But the split is essentially unchanged, coming in at 56%/44% this year.

That's more than amazing, given how decimated the homebuilders were during the recession. Existing home sales also dried up, yet home warranties continued to be sold and renewed. Appliance sales did dip in 2009 and again in 2011, but apparently not by enough to impact service contract sales. Apparently, in the face of uncertainty and adversity, the value of peace of mind increases, and protection plans can fill the need for predictable repair costs.

Total Service Contract Industry

Ten years after Consumer Reports first said "you don't need an extended warranty," it appears their advice was ignored. In the past decade, the two instances where the service contract industry shrank had little to do with the magazine's efforts. The recession hit car sales hard, and that hit VSC sales hard. But the advice of Consumer Reports did not affect VSC sales. Same goes for sales of electronics and appliances.

In Figure 7, we've combined all the sales data from Figures 3,4 and 6 into a single chart that details the size of the consumer product protection plan industry in the U.S. since 2006. And while it dipped from $29 billion in 2006 to $25.8 billion in 2009, it's grown every year since, to a total of $42.2 billion estimated for 2016.

The 10-year growth rate has been 258% for mobile phone protection plans sold by carriers, 55% for electronics service contracts sold by retailers, 49% for home warranties, and 43% for appliance service contracts sold by retailers. There was only 25% growth for VSCs sold by dealers, and the computer manufacturers who sold their service contracts direct to consumers saw a 17% decline.

Figure 7

US Service Contract Industry

Premiums Paid by Consumers, 2006 to 2016

(in US$ billions per year)

Of course, the car industry contracted during the recession, and that drastically reduced the number of VSC sales opportunities. The laptop industry also shrank as customers turned to smartphones. The difference is, the car industry came roaring back, setting a new unit sales record in 2015. The PC industry is in a permanent decline. In the appliance sector, not even the recession could slow down sales of protection plans, though growth has been very slight at times.

Expanding Coverage

The breadth and depth of protection plans is also growing. Car dealers now sell much more than mechanical breakdown coverage. Now they sell protection plans that cover dents and scratches, and even plans that protect owners from the cost of total losses and plans that prevent vehicle theft. Portable (and therefore droppable) electronics can be protected from not only accidental damage, but also from loss and theft.

And as feature phones and flip phones gave way to smartphones, the vulnerability increased and so did the protection revenue. There's nothing worse than a screen cracked in a spider-web shape on a $700 phone whose owner can't afford a repair. Or, as with GAP waivers, imagine a financed phone is lost or stolen, and its owner has to pay off that loan while financing a replacement.

All of these are perils that Consumer Reports didn't consider when it advised against buying break/fix coverage. We don't even call them extended warranties any more. Now they're protection plans, and they cover product owners from a long list of perils that have little to do with the cost or frequency of repairs. And now, 10 years later, the Consumer Reports advertisement seems more like a minor point than a turning point.