Wind Turbine Warranty Report:

It's been a tough few years for the largest global wind turbine manufacturers, revealing high warranty claims and accrual rates. Chinese companies have rapidly expanded their market share, while the European and American giants are attempting to streamline their businesses in the wake of some public product failures.

Wind power is a lucrative and fast-growing sector of the renewable energy industry. This is key infrastructure, and one of the most crucial elements of the global transition away from fossil fuels. According to the International Energy Agency (IEA)'s 2022 Wind Electricity Report, wind produced almost 1,900 terawatt-hours (TWh) of energy in 2021, up 17% from the year prior. Wind generates almost as much energy as all of the other renewables combined. The IEA estimates that wind power generation will need to continue to grow at a little more than this rate until 2030 in order to limit global temperature rise to 1.5 ℃ by 2050. This is in line with the United Nations' Intergovernmental Panel on Climate Change (IPCC)'s most recent guidelines to achieve net zero global CO₂ emissions by 2050. There is lots of room for error, and many caveats to these aims, which fall under UN Sustainable Development Goal (SDG) Seven: "Ensure access to affordable, reliable, sustainable and modern energy for all."

Many factors have contributed to the rapid growth of the wind industry. There is an underpinning of urgency in the transition from fossil fuels to renewable energy, which of course has driven development. Many governments around the world have implemented policies and incentives to encourage the development of wind power, including China and the United States, the two biggest polluters. This includes the many contracts for new wind farms awarded in the United States with funding from the 2021 Bipartisan Infrastructure Bill, which set aside $73 billion for "power infrastructure" with an emphasis on clean energy.

The industry has been scaling on two fronts: number of wind farms, and turbine size and efficiency. More turbines are being produced and installed, and the machines themselves continue to get bigger. There is obvious appeal to producing larger, lighter, and more aerodynamic blades. They are much more cost-effective, contributing to the steep decrease in the cost of each unit of wind-produced electricity.

Recently, one word in SDG 7 has been complicating things: reliable. This quick growth has left room for failure, with many questioning whether the industry has gotten "too big, too fast." According the Rachel Williamson's article "Wind turbine failure rates are rising -- has the industry gone too big, too fast?", "Advancements in materials, manufacturing and design techniques, and operations and maintenance tools led to a technical revolution in wind energy, allowing bigger and bigger machines to be installed. Wind turbines and their blades have rapidly been upsizing, with the average rotor diameter in the US reaching 127.5 metres in 2021, while the largest in the world is a 13.6 megawatt (MW) offshore wind turbine with a rotor diameter of 252 metres." Williamson asserts that this has directly led to "unexpected and increasing wind turbine failure rates, largely in newer and bigger models." She says that these product failures have been "savaging the profits of some of the world's biggest manufacturers, as Siemens Gamesa, GE and Vestas report heavy repair and maintenance losses."

Ryan Beene and Josh Saul concur. In their article "Wind Turbines Taller Than the Statue of Liberty Are Falling Over," Beene and Saul state that there has been "a rash of recent wind turbine malfunctions across the US and Europe, ranging from failures of key components to full collapses. Some industry veterans say they're happening more often, even if the events are occurring at only a small fraction of installed machines." They continue, "The race to add production lines for ever-bigger turbines is cited as a major culprit by people in the industry."

Of course, where there is a product failure, there is a warranty. So this wave of turbine malfunctions and collapses over the past couple of years is really a warranty story. This is particularly interesting because each warranty claim is from one business to another, e.g. a power company to a manufacturer. While each of the four companies we are tracking do have their own wind farms, they are also the major manufacturers selling turbines to many other global operators and power companies. This gets further complicated by the original manufacturers selling operations and maintenance agreements (O&Ms) and extended warranties to the buyers of the turbines, appealing since they usually only come with two- or five-year warranties and many reported malfunctions have been in older equipment. And since the technology has proved to be a bit accident-prone, many buyers are also insisting these contracts be backed by third-party insurance policies to guarantee service. With so many layers and involved parties, these warranties themselves can be quite complex.

In this article, we are taking a look at the warranty data for the world's four largest wind turbine manufacturers, Vestas Wind Systems A/S, General Electric Co., Siemens Energy AG, and Xinjiang Goldwind Science & Technology Co., Ltd. We analyzed all of their available annual reports since 2015, and extracted four metrics: the amount of warranty claims they paid, the amount of warranty accruals they made, the amount of warranty reserves they held, and the amount of product sales revenue they reported.

Vestas and Siemens both report their annual data in Euro, while GE reports in U.S. dollars, and Goldwind reports in Chinese Yuan. Especially considering currency fluctuations in the past few years, it is not possible to compare the metrics directly between the companies without using many conversions and estimates that confound the data. So we are going to look at each company individually, and analyze each company's claims and accruals totals compared to its product revenue. This gives us our two expense rates, warranty claims as a percent of sales (the claims rate) and warranty accruals as a percent of sales (the accrual rate).

Vestas

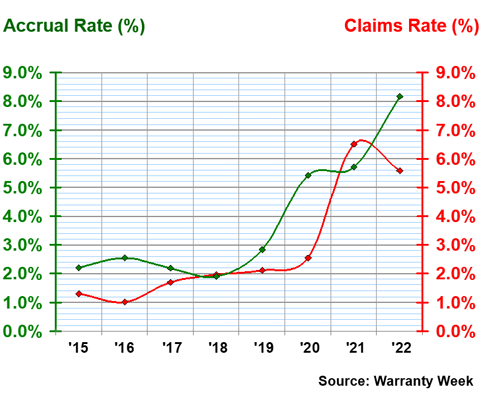

First, we will take a look at Vestas Wind Systems A/S, the Danish company that has been the largest wind turbine manufacturer in the world since 2013. Vestas' sole dedication is wind energy. It is mainly a manufacturer, but also provides service contracts for its own and other companies' turbines; service provided about one-fifth of its total 2022 revenue. Figure 1 shows Vestas' claims and accrual rates from 2015 to 2022.

Figure 1

Wind Turbine Manufacturer Warranties:

Vestas, Claims and Accrual Rates,

(as % of product revenue, 2015-2022)

Vestas' accrual rate jumped from 2.8% in 2019 to 5.4% in 2020. This seemed to be premonitory, since its claims rate jumped a year later, from 2.6% in 2020 to 6.5% in 2021. Typically, these rates stay below 5% except in extremely volatile cases.

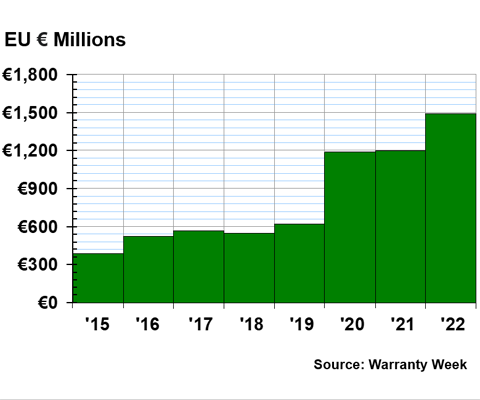

Vestas more than doubled its accruals between 2019 and 2020, from €72.8 million to €173.3 million. Accruals have remained elevated since then, increasing even further to €187 million in 2021, and €231.5 million in 2022. Meanwhile, claims more than doubled from 2020 to 2021, from €81.5 million to €213 million in just a year. Total claims fell a bit last year, to €158.3 million. As shown in Figure 1, although claims broke the upward trend in 2022, accruals continue to steadily increase. This is reflected in Vestas' warranty reserve balance, shown in Figure 2.

Figure 2

Wind Turbine Manufacturer Warranties:

Vestas, Warranty Reserve Balance,

(in millions of Euro, 2015-2022)

Figure 2 shows that the warranty reserve balance almost doubled between 2019 and 2020. So, in fact, a good portion of the big accrual in 2020 went right into the reserve account, rather than all going to pay claims. Yet keep in mind that Figure 1 shows us that this increase in accruals was not proportional to an increase in sales. There is a similar trend visible when comparing the 2022 data between Figures 1 and 2, with increased accruals leading to a larger reserve balance.

In their 2022 annual report, Vestas states, "The warranty provisions in 2022 included additional warranty provisions of EUR 124m due to increased repair costs caused by external cost inflation." Furthermore, they state that "the warranty costs were impacted by additional costs totalling EUR 93m related to the V164/V174 offshore technology recognised in the first quarter of 2022." Perhaps they are anticipating future warranty costs related to "increasing repair and upgrade costs," or specifically to offshore wind technology.

Beene and Saul report, "The Danish company says the supply chain wasn’t ready to handle the pace of product introductions by manufacturers, which has contributed to project delays, cost increases and quality challenges. 'We need a profitable and scalable wind industry to create a net-zero future, and this requires we continue to mature the entire value chain of renewables,' the company said in a statement."

On this note, Rachel Morison reported in January that Vestas' CEO Henrik Andersen said the company thinks wind turbines are big enough for now, and they will be focusing on expanding output rather than exponentially increasing the height and energy production potential of each individual turbine. After all, at a certain point, oversized turbine components become extremely cumbersome to transport. After some challenges, this seems like an acknowledgement from Vestas that it is better to refine the extant technology than to introduce a high margin for error. At the same time, they must remain competitive with the other major manufacturers in the industry.

General Electric

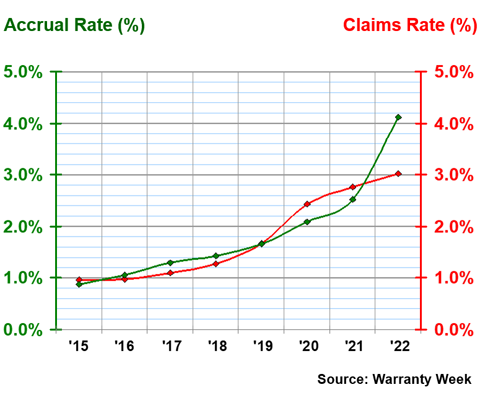

General Electric keeps its wind power under its subsidiary GE Renewable Energy, which is destined to spin off into its own company, GE Vernova, in 2024. As shown in Figure 3, its claims and accrual rates have been rising steadily since 2015, with the accrual rate spiking especially high in the past year.

Figure 3

Wind Turbine Manufacturer Warranties:

GE, Claims and Accrual Rates,

(as % of product revenue, 2015-2022)

The accrual rate jumped from 2.5% in 2021 to 4.1% in 2022. The claims rate in 2022 was 3.0%, slightly up from 2.8% the year prior. Though 2.8% does seem a bit high when contextualized against a claims rate of only 1.0% in 2015, these rates are notably lower than those of Vestas in recent years.

The big increase in accruals is significant. GE accrued $215.5 million in 2021, and stepped it up to $329.8 million in 2022. GE conveniently reports revenue numbers for each segment of its business separately, probably in anticipation of breaking into three distinct companies next year. In their 2022 annual report, they state that the renewable energy segment of their business lost "$1.5 billion organically, primarily attributable to Onshore Wind’s lower U.S. volume, higher warranty and related reserve charges of $0.5 billion in the third quarter of 2022 in response to the deployment of corrective measures and repair campaigns within our fleet, [...] and the impact of transitioning to newer product offerings internationally. Additionally, we observed cost inflation across all businesses and higher ramp up costs at Offshore Wind."

In his article "GE Is Likely to Keep Getting Windburned on Renewables," Thomas Black reports that "General Electric Co. plans to spend $600 million to try to right the ship at its wind-energy business, which is clearly the biggest drag on profits." According to Black, GE's CEO Larry Culp has also identified "the complexities of making too many variations for different customers" as a hindrance, and a top contributor to heightened warranty costs eating into profits. Instead, the company is pivoting to focusing on "what he calls workhorse products," a few standard models, with the aim of providing "higher quality while reducing costs." Hopefully, Black says, "With a simplified, more reliable wind turbine, the warranty costs will drop."

GE especially seems to feel some urgency here, probably due to the upcoming separation into three companies. Certainly, the $500 million accrual in the third quarter of 2022 just for costs related to wind turbine failures does not bode particularly well. But the company and its CEO seem very motivated to boost GE Renewable Energy's profitability.

It's important to note that we have yet to see claims heightened at the same rate as accruals for GE. In fact, on paper, it looks like around half of that $500 million went right into the reserve balance, at least for now. GE held $1.89 billion in warranty reserves at the end of 2021, and that balance increased to $2.15 billion at the end of 2022.

Goldwind

Next, we are going to take a look at China's largest wind turbine manufacturer, Goldwind. China has accounted for a growing share of the wind power industry over the past decade.

In his article "China widens renewable energy supply lead with wind power push," Gavin Maguire reports that "China has been the world's largest and fastest-growing producer of renewable energy for more than a decade, but has widened its lead over international rivals through a steep acceleration in the roll out of wind capacity since 2021." In 2022, China "generated 46% more wind power than all of Europe." Europe was the largest global wind power producer until 2020, when it was surpassed by China. 34% of China's electricity came from renewable sources in 2022. In short, China has rushed past Europe and the United States in wind power generation in the past two years, growing much faster than other regions.

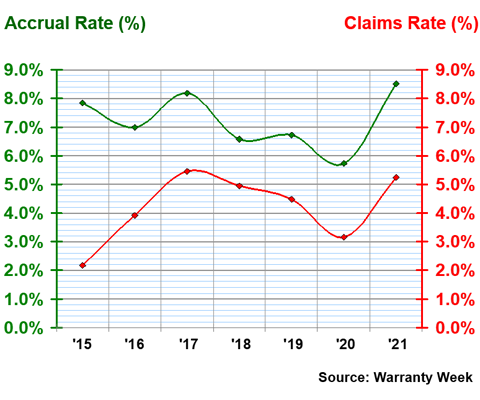

Figure 4 shows Goldwind's claims and accrual rates from 2015 to 2021. The company has yet to release its 2022 annual report.

Figure 4

Wind Turbine Manufacturer Warranties:

Goldwind, Claims and Accrual Rates,

(as % of product revenue, 2015-2021)

Goldwind is distinct from Vestas and GE because its accrual rate always remains higher than its claims rate. It is also unique because of how high these rates have remained. The company had a 8.5% accrual rate in 2021, up from 5.7% in 2020. The claims rate also increased to 5.2% in 2021, up from 3.2% the year prior. However, these are not records for the company. As we see in Figure 4, both rates were similarly high in 2017. The claims rate was 5.5% that year, and the accrual rate was 8.2%.

It is seriously remarkable that Goldwind has maintained an accrual rate above 5% for almost a decade. With that said, its claims rate also hovers rather high, and has tended to fluctuate enough to justify the heightened accruals. Goldwind's warranty reserve balance has been steadily increasing for the past four years. While the claims and accrual rates both went up in 2021, reserves also reached a record high of 4.99 billion Yuan.

Despite these high expense rates, there is not much news about specific product failures or challenges for Goldwind. In fact, much of the coverage of China's wind power industry is overwhelmingly positive. It remains to be seen how these very high warranty expenses proportional to sales will impact revenue and future product design and implementation. And perhaps we should give kudos to the other three companies in this report, for publicly addressing product malfunctions and explaining their lump sum accruals in their annual reports.

Siemens Energy

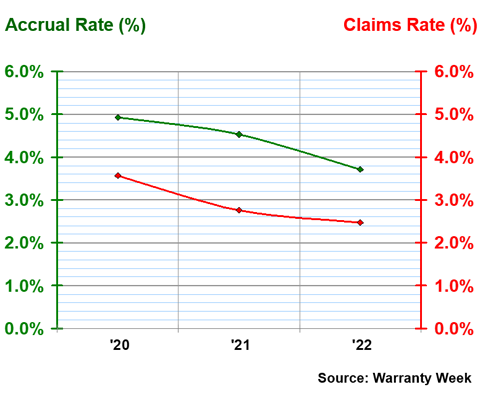

Finally, we will take a look at Siemens Energy's expense rates from 2020 to 2022. Unfortunately, these data are not available from earlier than 2020 due to a lot of restructuring. Siemens Energy was created as an independent company in April 2020, out of the energy division of Siemens AG. In turn, Siemens Energy is a 93% owner of Siemens Gamesa Renewable Energy SA (SGRE), which was originally a division of Siemens formed through the 2016 merger of Siemens Wind Power and Gamesa. To make things a little less complicated, there have been reports that Siemens Gamesa is preparing to delist from the stock market and fully merge with Siemens Energy.

Figure 5

Wind Turbine Manufacturer Warranties:

Siemens Energy, Claims and Accrual Rates,

(as % of product revenue, 2020-2022)

Though it is difficult to wrap one's head around trends based only on three years of data, it is clear that the two expense rates have been decreasing over the past few years. The claims rate was down to 2.5% in 2022, from 2.8% in 2021, and 3.6% in 2020. The accrual rate decreased from 4.9% in 2020, to 4.5% in 2021, to 3.7% in 2022.

In their 2022 annual report, Siemens Energy reported, "As in the previous year, the increase in the provision for contingent losses is mainly due to deviations at SGRE in Brazil, North of Europe and North America mainly related to the SG 5.X product development affecting ongoing projects as well as to other increases in estimated costs in projects. As of September 30, 2022, this resulted in a provision for contingent losses of €455 million."

It seems like all three major Western wind turbine manufacturers are in consensus and following the same advice. Beene and Saul report, "Siemens Gamesa’s CEO Jochen Eickholt has told investors the company is working to increase standardization among its products, to prune a portfolio that had become too broad." Perhaps they were in a reverie, competing with each other to see who could create the biggest, tallest, newest wind turbine. But the wind power industry has shown us that too much innovation too quickly can be a bad thing, resulting in too many products and a lot of room for glitches and failures to fall through the cracks. Meanwhile, Chinese manufacturers have been taking on a rapidly increasing market share; it is unclear if this share of the market will face similar challenges.

In an interview with CNBC, Siemens Energy CEO Christian Bruch said, "There’s no question -- if we don’t resolve it as an industry, we are missing a substantial part of the energy transition, and we’ll fail with the energy transition. So there’s no option but to fix it." Certainly, this reflects the urgency currently felt within the wind power industry, both to cut warranty costs and boost profits for each company, and to spur on the global transition to renewable energy overall. It seems there is hope yet, as the major players have all identified the same fatal flaw, and are taking steps to mitigate the heightened warranty expenses shown in this report.